What Is a Hard Credit Pull?

When you apply for credit, such as a loan, credit card, or financing program, the lender often performs a hard credit pull (also known as a hard inquiry). This is a way for lenders to assess your credit history and determine whether you are a good candidate for borrowing.

But what exactly does that mean for your credit score? Let’s dive into what a hard pull is, how it works, and what you need to know before applying.

Hard Pull vs. Soft Pull: What’s the Difference?

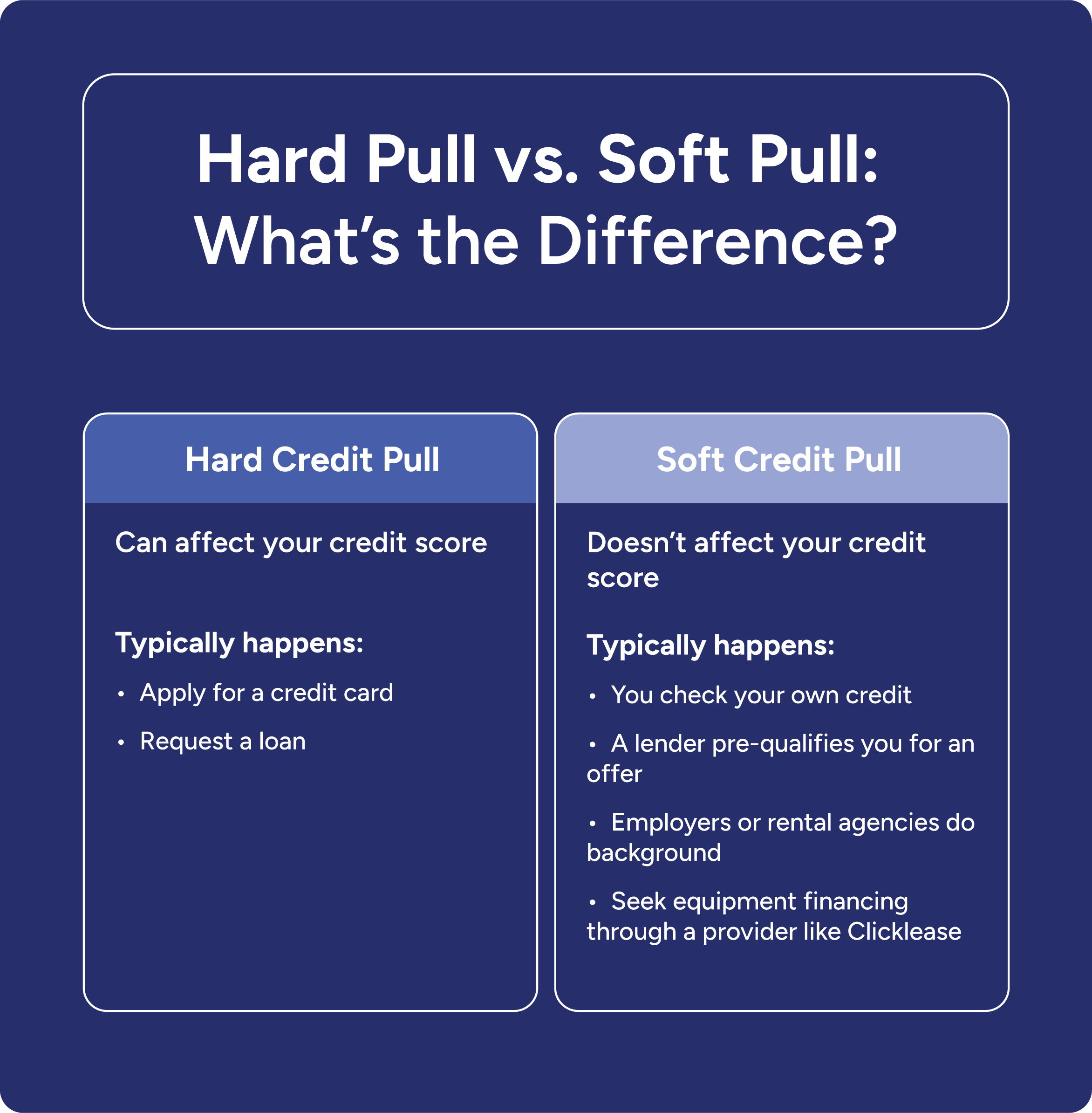

A hard credit pull occurs when a lender reviews your credit report as part of a lending decision. This typically happens when you:

- Apply for a credit card

- Request a loan

A soft credit pull, on the other hand, happens when:

- You check your own credit

- A lender pre-qualifies you for an offer

- Employers or rental agencies do background checks

- Seek equipment financing through a provider like Clicklease

Soft pulls do not affect your credit score. Hard pulls can, but usually only slightly and temporarily.

Does a Hard Pull Affect Your Credit?

Yes, a hard credit pull can impact your credit score, but the effect is usually small. Most hard inquiries lower your score by five points or less. If you have a strong credit history, the impact may be barely noticeable.

However, multiple hard pulls in a short period of time can have a greater effect. Lenders may see this as a sign you are taking on a lot of new debt.

How Long Does a Hard Credit Pull Last?

A hard inquiry remains on your credit report for two years, but it typically affects your credit score for only 12 months. Over time, the impact fades, especially if you maintain good credit habits like making payments on time.

Do Credit Cards Do a Hard Pull?

Yes. Almost every time you apply for a credit card, the issuer will run a hard credit check. That is why it is important to apply only for credit cards you are likely to qualify for.

How Do Credit Bureaus Handle Hard Pulls?

There are three major credit bureaus: Experian, Equifax, and TransUnion. Lenders can report to any one or more of them, which means your credit score might vary depending on which bureau’s data is being used.

Each bureau may show slightly different information, including your credit score number and timing of hard inquiries. This is completely normal, but it’s helpful to keep track of your reports across all three.

When Does Clicklease Use a Hard or Soft Pull?

At Clicklease, we do a soft credit pull, checking your eligibility will not affect your credit score.

This approach gives you or your customers the power to explore equipment financing options without any risk to your credit.

Check your lease eligibility with no credit impact

Key Takeaways

- A hard credit pull is a credit check that happens when you apply for a new credit product or loan.

- It may slightly lower your credit score, usually by fewer than five points.

- The inquiry remains on your credit report for up to two years but only impacts your score for one year.

- Soft pulls do not affect your credit and are used for pre-approvals or self-checks.

- Clicklease uses a soft credit score pull to get you started, giving you a risk-free way to explore equipment financing.

Need Equipment Financing?

Clicklease helps small businesses get the tools they need to grow. You can qualify for a lease in minutes without affecting your credit.